The Indian government has initiated a fundamental overhaul of its regulatory structure governing deep technology enterprises, signaling a strategic national commitment to cultivating long-horizon, science-led innovation. Recognizing the inherent disparity between the rapid growth cycles of conventional digital startups and the extended maturation periods required for breakthrough technologies—particularly in critical sectors like space, semiconductors, advanced manufacturing, and biotechnology—New Delhi has significantly adjusted its policy framework. This comprehensive reform package, blending regulatory relief with the strategic deployment of public capital, is designed to nurture these foundational ventures through their often decade-long journey from laboratory concept to commercial viability.

Central to this policy shift is the doubling of the period for which deep tech companies qualify for "startup" status. Previously capped at ten years, this eligibility window has now been extended to twenty years. This single change carries profound implications, allowing these companies to benefit from crucial startup-specific tax exemptions, grants, and streamlined regulatory compliance for a much longer duration. Complementing this timeline extension, the government also tripled the maximum annual revenue threshold for retaining these benefits, raising it from ₹1 billion (approximately $11.04 million) to ₹3 billion (about $33.12 million). These adjustments directly address a major structural weakness in the previous ecosystem, where science- and engineering-intensive businesses often found themselves prematurely "graduating" out of support mechanisms while still pre-commercial, heavily reliant on R&D, and far from achieving sustainable scale.

The Imperative for Patient Capital

Deep technology, defined by its reliance on tangible scientific discovery or engineering innovation, operates under entirely different economic constraints than asset-light, consumer-focused internet platforms. Developing a novel therapeutic drug, building a satellite constellation, or fabricating advanced semiconductor materials requires massive upfront capital expenditure, years of laboratory validation (often tracked via Technology Readiness Levels, or TRLs), navigating complex intellectual property landscapes, and lengthy regulatory approval processes.

Under the prior framework, the finite ten-year window imposed an artificial pressure point on founders. Vishesh Rajaram, a founding partner at deep tech venture capital firm Speciale Invest, characterized this situation as creating a "false failure signal." Companies were being judged against a policy timeline rather than against genuine technological progress. A pre-revenue biotech firm or a fledgling space propulsion company nearing its fifth year faced the existential threat of losing its hard-won startup status—and the associated tax holidays—precisely when it needed patient capital and stable regulatory support the most. This misalignment often forced deep tech founders to prioritize rapid, often suboptimal, commercialization attempts over rigorous, long-term R&D, or even worse, incentivized them to move their intellectual property and headquarters to jurisdictions with more accommodating capital and regulatory environments.

By formally recognizing the unique nature of deep tech ventures, the government aims to de-risk these long incubation periods. This policy validation reduces critical friction points in the operational reality of founders, streamlining interactions with state agencies and significantly improving the narrative for long-term fundraising and follow-on capital deployment.

Combining Regulatory Reform with Sovereign Finance

This regulatory overhaul is not an isolated measure; it is tightly coupled with New Delhi’s broader strategy to leverage public capital for strategic technological advancement. The cornerstone of this financial strategy is the ₹1 trillion (around $11 billion) Research, Development and Innovation Fund (RDI Fund), announced last year and now moving into operationalization.

The RDI Fund is explicitly designed to address the chronic funding gaps that plague capital-intensive deep tech companies beyond the early stages—a period often referred to as the "valley of death" between successful proof-of-concept and market scale-up. Investors, including those active in the Indian market, consistently point out that while seed-stage capital has become more accessible, the true binding constraint remains the funding depth required for Series A, B, and growth rounds, particularly for businesses demanding specialized infrastructure, large production facilities, or extended clinical trials.

Arun Kumar, managing partner at Celesta Capital, emphasized that the RDI framework’s primary benefit is injecting much-needed patient capital at critical growth junctures. Crucially, the fund is structured not merely as a passive fund-of-funds. While it routes public capital through established venture funds, providing them with similar long-term tenors as private capital, the RDI vehicle is also mandated to provide direct credit lines, grants, and even take equity positions in strategic deep tech startups. This multifaceted approach is intended to expand the overall capital pool without distorting the commercial due diligence processes that govern private investment decisions. It functions as a catalytic nucleus, attracting greater private capital formation around nationally significant projects.

Mitigating the ‘Graduation Cliff’ and Investor Confidence

The concept of avoiding a "graduation cliff"—where regulatory support abruptly ceases just as a company enters its high-growth phase—is central to the new framework’s philosophy. Siddarth Pai, founding partner at 3one4 Capital and co-chair of regulatory affairs at the Indian Venture and Alternate Capital Association, noted that this extended runway ensures companies are not cut off from vital support when they are most vulnerable and scaling rapidly.

For institutional investors, both domestic and global, this regulatory stability is arguably as important as the immediate financial benefits. Deep tech investment inherently requires a long-term perspective, often operating on seven-to-twelve-year horizons before substantial returns are realized. Pratik Agarwal, a partner at Accel, observed that the 20-year lifecycle recognition provides investors with significantly greater confidence that the policy environment will remain supportive throughout the company’s entire developmental journey. This stability mitigates policy risk, which has historically been a deterrent for large, global funds contemplating massive, long-duration allocations into Indian frontier technologies. Agarwal suggested that this shift reflects India’s commitment to learning from successful long-term innovation frameworks implemented in the U.S. and Europe, which prioritize creating patient capital environments for disruptive, frontier building.

The private market has responded with complementary initiatives. A coalition of major U.S. and Indian venture firms recently launched the India Deep Tech Alliance, a consortium committed to deploying over $1 billion into the country’s deep tech ecosystem. This alliance, which includes prominent names like Accel, Blume Ventures, Celesta Capital, and Qualcomm Ventures, with chip giant Nvidia acting as an advisor, demonstrates a strong belief that the regulatory and financial groundwork laid by the government is sufficient to support scaled private investment.

Global Disparity and Sectoral Momentum

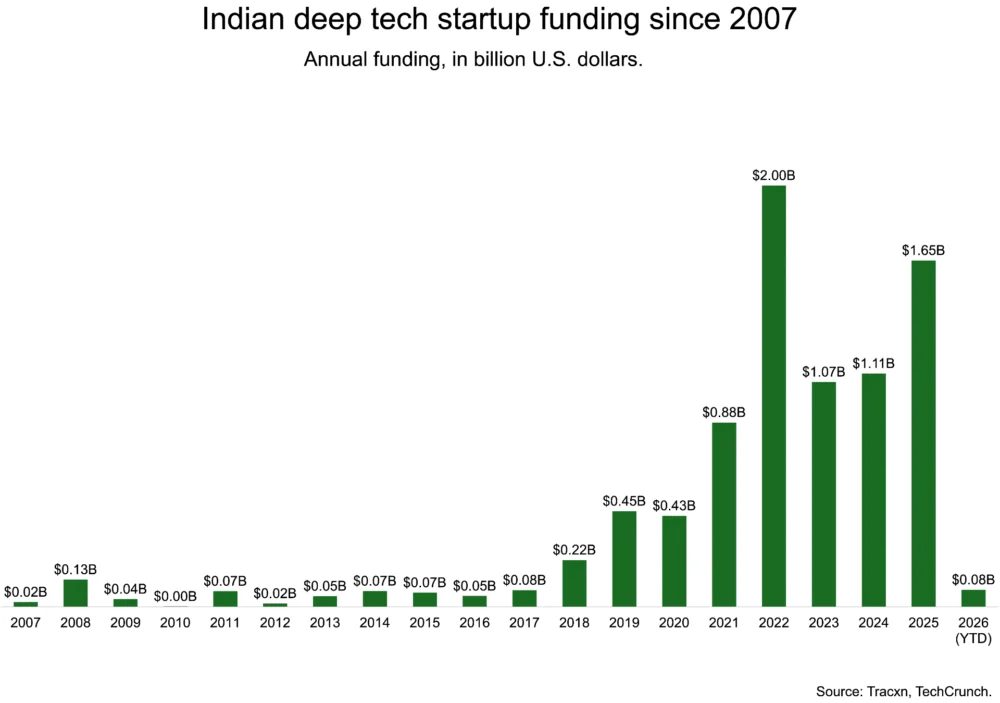

While the policy intent is ambitious, the current scale of the Indian deep tech market underscores the magnitude of the challenge. Historically, the total funding raised by Indian deep tech startups stands at approximately $8.54 billion. Although recent momentum is positive—funding rebounded sharply to $1.65 billion in 2025, up from $1.1 billion in the preceding two years—this figure pales in comparison to global peers. Data shows that U.S. deep tech startups secured approximately $147 billion in 2025, while China accounted for roughly $81 billion in the same period.

This vast disparity highlights that India, despite its immense pool of engineering and scientific talent, still faces structural hurdles in mobilizing the sheer capital density required for truly capital-intensive technologies like advanced semiconductor fabrication or large-scale quantum computing efforts.

However, the recent funding recovery suggests a targeted shift toward longer-horizon investing, aligning with specific national priorities. Investor confidence is growing particularly in areas deemed strategically important by the government, including defense technology, advanced manufacturing, climate technologies (e.g., green hydrogen, carbon capture), and the semiconductor value chain. Neha Singh, co-founder of Tracxn, noted that this pickup in funding is indicative of a systemic move by venture capital toward recognizing and backing ventures that demand a sustained, patient approach.

Future Implications: Addressing the ‘Flipping’ Phenomenon

A key future indicator of the success of this policy framework will be its ability to reduce the tendency of successful Indian startups—known as "flipping"—to relocate their headquarters overseas (typically to Singapore, the U.S., or the Netherlands) as they seek larger capital rounds, better regulatory predictability, and access to massive global customers.

The extended 20-year runway strengthens the fundamental case for building and scaling in India. By guaranteeing regulatory benefits across the entire development lifecycle, the government removes a major incentive for early migration. While access to late-stage global capital and major procurement contracts will always influence ultimate scaling decisions, the domestic landscape is evolving favorably. India’s public markets have shown a dramatically increased appetite for venture-backed technology companies over the past five years, making domestic Initial Public Offerings (IPOs) a far more credible and attractive exit option than they were previously. This growing maturity in the domestic capital markets provides a powerful counter-incentive to incorporating overseas.

Furthermore, the operationalization of the RDI Fund and the subsequent crowding-in of private capital are anticipated to address the late-stage funding shortage, making India a more comprehensive scaling environment. The goal is to move beyond simply supporting innovation to actively supporting the industrialization of those innovations within the country’s borders.

The ultimate assessment of this policy framework, however, rests on tangible, globally competitive outcomes. For investors who commit capital over decade-long cycles, the true signal of success will be the emergence of a critical mass of Indian deep tech companies that not only succeed domestically but also dominate on the world stage. Arun Kumar of Celesta Capital established a clear benchmark: the sustained success of ten globally competitive deep tech companies originating from India over the next decade would definitively signal the maturity and effectiveness of this long-term ecosystem development strategy. This transformation is not merely about tax breaks; it is about establishing India as a sovereign hub for frontier technology that can compete with established innovation economies.