The honeymoon phase of "growth at any cost" in the world’s most populous digital market is reaching a definitive conclusion. For the past two years, Silicon Valley’s artificial intelligence titans have treated the Indian subcontinent as a vast laboratory for user acquisition, flooding the market with subsidized premium access and aggressive promotional bundles. However, as 2026 unfolds, a strategic pivot is underway. The industry is moving away from the "free-to-play" model that defined the early generative AI (GenAI) boom, transitioning toward a rigorous test of whether India’s massive user base can be converted into a sustainable revenue engine.

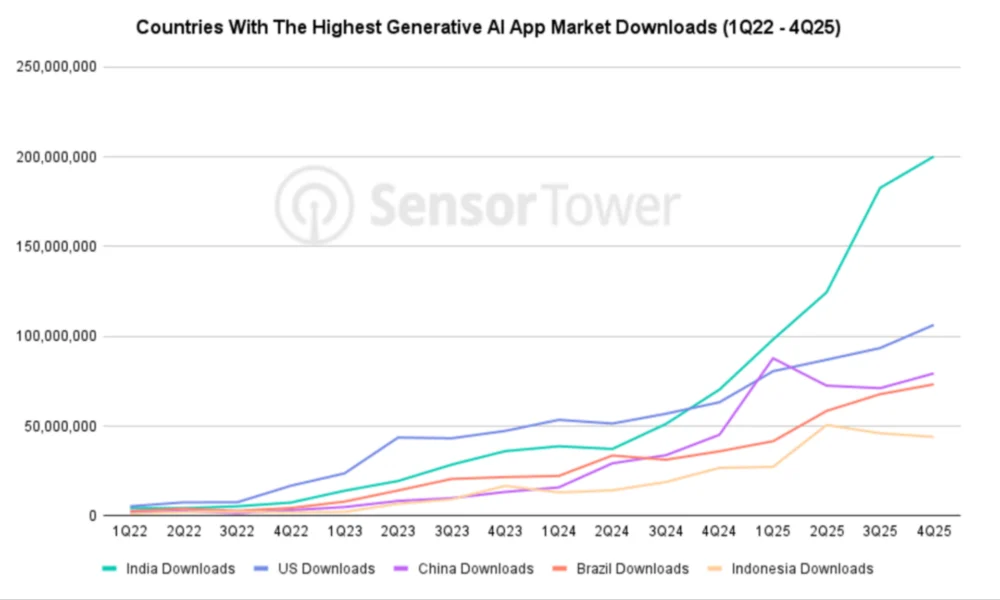

This shift comes at a critical juncture. According to the latest data from market intelligence firm Sensor Tower, India solidified its position as the global leader in generative AI app downloads in 2025. With a staggering 207% year-over-year increase in installations, India has effectively outpaced the United States, commanding roughly 20% of all global GenAI app downloads. Yet, this dominance in volume is starkly contrasted by a lag in value. Despite driving a fifth of the world’s downloads, India accounts for a mere 1% of global in-app purchase revenue in the sector. This "monetization gap" is now the primary challenge for companies like OpenAI, Google, and Perplexity as they sunset the promotional offers that fueled their initial ascent.

The scale of the Indian opportunity is undeniable, a fact punctuated by the high-profile presence of global tech leaders at a major AI summit in New Delhi recently. The convergence of OpenAI’s Sam Altman, Anthropic’s Dario Amodei, and Alphabet CEO Sundar Pichai in the Indian capital signals that the country is no longer viewed merely as a source of low-cost engineering talent, but as the ultimate battleground for AI supremacy. For these firms, the mission is twofold: to embed their models into the daily workflows of a billion-plus internet users and to navigate the unique price sensitivities of the Indian consumer.

To achieve the first goal, the industry’s heavyweights spent 2025 engaged in a blitz of subsidies. OpenAI introduced "ChatGPT Go," a localized, sub-$5 tier designed to lower the barrier to entry, while Google leveraged its partnership with Reliance Jio to provide Pro-level AI access to millions of mobile users. Perplexity AI similarly utilized a strategic alliance with Airtel to bundle its premium search capabilities with data plans. These moves were calculated gambles, designed to build "muscle memory" among users before the inevitable introduction of paywalls.

The data suggests that while the "growth" part of the gamble paid off, the "revenue" part remains elusive. In the final months of 2025, even as downloads peaked, in-app purchase revenue in India actually contracted—falling 22% in November and 18% in December. ChatGPT, which holds a commanding 60% share of the local market’s AI revenue, saw an even sharper decline of over 30% during that period. This paradox was largely the result of the very promotions intended to hook users; by offering premium features for free or at a steep discount, companies effectively suppressed their own short-term earning potential to secure long-term market share.

Now, the bill is coming due. Perplexity’s bundled offer with Airtel expired in January, and OpenAI’s ChatGPT Go promotions have largely been phased out. This sets the stage for a "moment of truth" in 2026. Can these platforms maintain their massive Monthly Active User (MAU) counts when the price of admission rises? As of early 2026, the leaderboard remains top-heavy: ChatGPT leads with 180 million MAUs, followed by Google’s Gemini at 118 million. Perplexity and Meta AI follow at 19 million and 12 million, respectively.

The challenge of monetizing the Indian user is rooted in both economic and behavioral factors. Historically, Indian consumers have shown a high degree of "value consciousness," a trait that forced the streaming and SaaS industries to adopt hyper-localized pricing. In the U.S., a $20 monthly subscription for an AI assistant is often seen as a marginal expense for a productivity tool. In India, that same price point competes with a household’s monthly grocery bill or high-speed fiber internet connection.

Furthermore, engagement metrics reveal a maturity gap. Sensor Tower’s analysis indicates that U.S. users spend 21% more time per week on AI apps and log 17% more sessions than their Indian counterparts. This suggests that while Indians are downloading these tools in record numbers, they may not yet be integrating them into their professional or personal lives with the same intensity as users in more established markets. For a subscription model to work, the "utility-to-cost" ratio must be undeniable. If the AI is seen merely as a novelty for generating viral images or casual queries, the churn rate following the end of promotions will be catastrophic.

To combat this, analysts suggest that AI firms must look beyond the standard monthly subscription model. Sneha Pandey, an insights analyst at Sensor Tower, notes that the future of Indian AI monetization likely lies in "sachet pricing"—a term borrowed from the Indian FMCG sector where products like shampoo are sold in small, affordable packets. In the digital realm, this translates to micro-transactions, daily passes, or deeply integrated telecom bundles. By breaking down the cost into smaller, more digestible units, firms can cater to the country’s young, mobile-first demographic without requiring a long-term financial commitment.

Beyond the consumer market, the real prize may lie in India’s burgeoning enterprise and developer ecosystems. The surge in downloads in 2025 was driven not just by chatbots, but by content creation and editing tools, which accounted for seven of the top 20 GenAI apps. This indicates a massive "prosumer" class—freelancers, content creators, and small business owners—who are using AI to compete in the global gig economy. For this segment, AI is a capital investment rather than a luxury, making them far more likely to convert to paid tiers if the tools offer a clear ROI.

The entry of new players like DeepSeek and Grok, alongside upgrades to existing models like Claude and Meta AI, has further commoditized basic LLM capabilities. This creates a "race to the bottom" on pricing for general-purpose chatbots, forcing leaders like OpenAI and Google to differentiate through ecosystem lock-in. Google’s integration of Gemini into the Android operating system and Workspace suite gives it a structural advantage in India’s smartphone-heavy market. Conversely, OpenAI’s brand equity and its move to establish a local presence in India suggest it is prepared for a long-term war of attrition.

Looking ahead, the trajectory of India’s AI economy will likely mirror the "Jio effect" seen in the telecom sector a decade ago. Initial years of free data led to a total transformation of the digital landscape, followed by a gradual but steady increase in Average Revenue Per User (ARPU). For AI firms, the current dip in revenue is a necessary byproduct of the transition from a "discovery" phase to a "utility" phase.

However, the road to profitability will require more than just patience. It will require localized innovation. The next wave of growth in India will likely be driven by "Indic" LLMs—models trained specifically on India’s diverse linguistic and cultural nuances. While the global giants provide the foundational infrastructure, the apps that ultimately win the hearts (and wallets) of Indian users will be those that can navigate the complexities of Hinglish, Tamil, or Bengali with the same fluency as English.

As the industry moves deeper into 2026, the focus will shift from the "how many" to the "how much." The 180 million monthly active users on ChatGPT represent a gold mine of data and potential, but they also represent a massive server cost. In a world where venture capital is increasingly demanding a path to profitability, the pressure on AI firms to turn Indian downloads into dollars has never been higher. The promotional era provided the spark; now, the industry must prove it can sustain the fire in one of the world’s most competitive and price-sensitive markets. The outcome of this experiment will not only determine the future of the Indian tech landscape but will provide a blueprint for AI monetization across the entire developing world.